Your Word Was Your Credit Line: How Main Street Ran on Promises Before Plastic

Walk into any small-town general store in 1950s America, and you'd witness something that would seem impossible today: customers walking out with groceries, tools, and household goods without paying a dime upfront. No credit cards, no background checks, no signature loans—just a merchant's scrawled notation in a worn ledger book and the unspoken promise that payment would come when the harvest was in or the paycheck arrived.

This was America's original credit system, and it ran on something banks today spend billions trying to measure: trust.

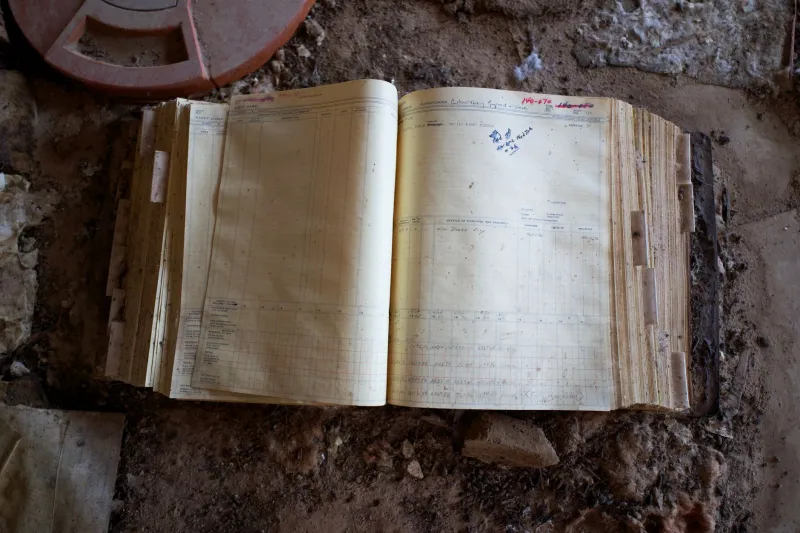

The Ledger Book Economy

Every corner store, feed shop, and pharmacy kept what locals called "the book"—a thick ledger where merchants tracked who owed what. Mrs. Henderson might owe $12.50 for last month's groceries. Tom Williams had a running tab for hardware supplies that stretched back three months. The blacksmith carried half the town's horseshoeing bills on his books, knowing farmers would settle up after selling their crops.

Photo: Tom Williams, via is1-ssl.mzstatic.com

Photo: Tom Williams, via is1-ssl.mzstatic.com

These weren't formal loans with interest rates and payment schedules. They were community agreements based on intimate knowledge of each customer's character, work ethic, and family situation. The merchant knew who always paid eventually, who needed gentle reminders, and who might struggle but would make good given time.

"Put it on my account" was America's most common transaction, and it worked because everyone involved understood the stakes. Your credit wasn't a number—it was your reputation walking around town.

When Everyone Knew Everyone's Business

This system thrived because small-town America operated on complete transparency. If you stiffed the grocer, everyone knew by Sunday service. If you were struggling to pay bills, the whole community understood why. There was no anonymity, no hiding behind corporate policies or automated systems.

Merchants made credit decisions based on factors no algorithm could capture. They knew whose husband had steady work at the mill, whose crop looked promising this year, whose family helped neighbors during hard times. They extended credit to the widow struggling to feed her children and cut off the bachelor who spent his wages at the tavern.

This personal knowledge created a surprisingly efficient system. Default rates were often lower than modern credit cards, not because people were more honest, but because the social cost of not paying was enormous. Your financial reputation affected everything from your children's marriage prospects to your standing at church.

The Mechanics of Trust

The beauty of the ledger system was its simplicity. When you needed something, you asked to "put it on account." The merchant wrote your name, the items, and the amount in their book. At the end of the month—or when you got paid—you settled up, usually in cash.

Some merchants offered informal payment plans for big purchases. A new plow might be paid off over several months, timed to harvest seasons. Wedding dresses were often bought on credit and paid for with wedding gift money. Even medical bills followed this pattern, with doctors carrying patients on their books indefinitely if necessary.

Interest was rare and usually informal—maybe an extra dollar added to a long-overdue account, or a small discount for prompt payment. The real currency was relationship maintenance, not profit maximization.

The Dark Side of Personal Credit

But this system had serious flaws that modern credit, for all its impersonal complexity, has largely eliminated. Merchant credit was inherently discriminatory. Your access to credit depended entirely on how the store owner perceived you, your family, your race, your religion, and your place in the social hierarchy.

Wealthy families got unlimited credit at favorable terms. Working families got basic necessities on reasonable terms. But outsiders, minorities, or anyone who didn't fit the community's social expectations might find credit denied entirely, regardless of their ability to pay.

There was no appeals process, no regulatory oversight, no way to shop around for better terms. If the town's only grocer decided you were a credit risk, you paid cash or went hungry.

The Modern Credit Revolution

Today's credit system—with its credit scores, background checks, and standardized terms—seems coldly impersonal by comparison. But it's also remarkably democratic. Your FICO score doesn't care about your family name, your church attendance, or whether the banker likes your politics. It's based purely on your payment history and financial behavior.

We've traded personal relationships for mathematical precision, local knowledge for standardized algorithms, and community accountability for legal enforcement. A modern credit card gives you access to instant credit anywhere in the world, but you'll never have the relationship with Chase Bank that your grandfather had with the corner grocer.

What We Lost in Translation

The shift from personal to institutional credit reflects a broader change in American life—from tight-knit communities where everyone knew your story to anonymous urban societies where your credit score tells strangers everything they need to know about your financial trustworthiness.

We gained efficiency, fairness, and access. We lost the human element that made credit feel like community support rather than corporate profit-seeking. The merchant who carried your family through a tough winter has been replaced by automated systems that approve or deny based on data points and risk models.

The handshake deals that built Main Street couldn't survive in a mobile, anonymous society. But sometimes, when you're dealing with another automated phone system or fighting a credit score error, you might wonder if we gained as much as we lost in the translation.

Photo: Main Street, via img.freepik.com

Photo: Main Street, via img.freepik.com